The following is the first part of a series of posts and is based on a white paper that provides more detail. Under the section header “The Growing Investor Demand for Climate-Related Risk Disclosure and Related Information” within the proposed rule, SEC begins to build the case by citing a long discussion of organizations and the various international initiatives, citing to the:

The list and assets under management appear very compelling, if not overwhelming. However, SEC has failed to provide context. How many investors are represented multiple times in the laundry list, signing onto multiple of these initiatives? Perhaps those investors are promiscuous joiners, signing onto multiple of these initiatives. Indeed, in Footnote 56 of the rule SEC acknowledges, “There is some overlap in the signatories to the listed initiatives.” It is not clear what the overlap is in terms of both number of investors and total assets managed, but perhaps that obfuscation is intended. Digging deeper into the numbers SEC cites, there are seven main climate change non-profit advocacy organizations behind them:

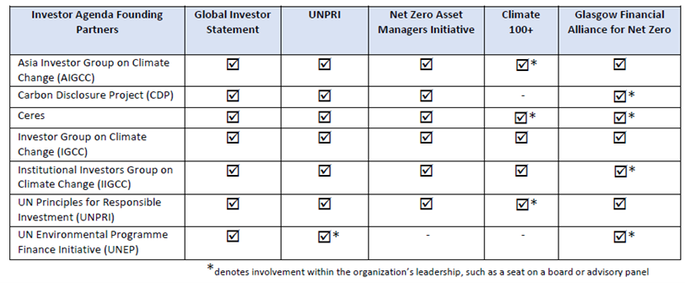

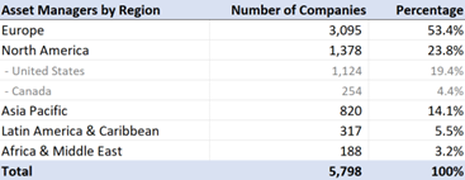

An examination of how these groups are interrelated further calls into question any broad consensus for climate disclosure. The multiple international groups cited by SEC are not operating independently from each other, but rather are working in close collaboration. The following chart shows that, across the board, each initiative is comprised of the same small group of members. There is very little to differentiate the Global Investor Statement from the Net Zero Asset Managers Initiative or from any of the others. These groups are so intertwined that it is not at all clear they represent anything other than a minority of investors advancing a particular policy agenda. Intertwined Network of Climate Initiatives Cited by SEC and Non-Profit Advocacy Group  However intertwined these groups and initiatives are, a more fundamentally fatal flaw in the use of their work by SEC is the fact that the vast majority of investors they represent are foreign. Across those seven climate initiatives and the global network of non-profit organizations that support them, only 19% are American. More than half are European. Asset Management Companies Supporting Climate Activis  Western Energy Alliance analyzed data on the 6,991 companies included in these initiatives, For the 5,800 companies that provide country-of-origin locations, a more than representative sample, only 1,124 are American. Foreign companies do not set United States policy. SEC is skating on very thin ice when it uses foreign companies organized into initiatives by seven climate change activist organizations to justify a regulation that would impose a $10.235 billion cost on American society. Further diving into the numbers, the 1,124 American asset management companies participating in the climate change disclosure advocacy that these seven groups are orchestrating represent a mere 7% of the 16,127 registered investment companies in the United States. Therefore, SEC’s implied “consensus” of investment companies clamoring for disclosure falls apart at just 7%. That is pretty thin ice for a rule with such wide-ranging implications. It's concerning that the SEC is justifying this proposed rule by citing to these global climate initiatives. SEC wants the public to focus on the trillions of dollars and thousands of asset managers these initiatives represent around the world. Yet, the agency is overlooking the fact that these groups vastly represent foreign interests and a global network of activists, not a majority of American investors. More details on this topic and several other shortcomings of SEC’s climate disclosure rule are available in our white paper. This is the first in a series of posts on SEC's climate disclosure rule. Read the next post here.

Comments are closed.

|

Archives

June 2024

Categories |

RSS Feed

RSS Feed